The digital finance download: Diplomats and journalists explore the data driving financial inclusion in the future global economy

On the morning of November 17, Meridian International Center hosted the first session of its newest convening series, The Digital Finance Future: Inclusive and Global Economic Growth. Over breakfast, 22 journalists, diplomats and digital finance experts gathered for a roundtable discussion on the role of digital services in creating a more inclusive global economy.

Meridian’s President and CEO Ambassador Stuart Holliday welcomed the group with thoughts on the state of the global economy. "When we think about the world today – in terms of inequality, income and the uncertainty around migration in countries – economic stability is so important." The digital revolution has become part of that equation, opening up access to banking and financial tools for 500 million people in the past five years alone. Yet billions of people worldwide are still unbanked. While we are beginning to see change toward greater financial inclusion, there is a long path ahead that requires action from governments, regulators, policymakers, consumers, humanitarians and business leaders around the globe.

To demonstrate the need for cross-sector collaboration in the future digital economy, Rosita Najmi, Program Officer at the Bill & Melinda Gates Foundation, facilitated a group exercise on digital financial services. Holding up a wallet, just like the ones most people carry around today, Rosita prompted the participants to examine the wallets in front of them. “Take a good look because these wallets are among the last of their kind.” The financial industry is transforming as physical money and manual transactions are digitized – not because digital is trendy but because digital financial services have benefits and advantages, particularly for the poor. Not all lives have equal opportunity today but digital tools and services are helping to reduce the cost of financial inclusion in order to create a future economy that benefits everyone.

Inside each wallet was a set of assets that included everything from a mobile phone, which symbolizes how digital money can go more places more quickly and more securely than cash, to an identification card, which 1.5 billion people worldwide lack today – a major barrier to accessing vital financial services. Najmi called the participants’ attention to a "24" bill, representing the average number of people forced to flee their homes every minute. She described the growing importance of humanitarian responses that safely assist with money transfers across borders. "My family came to the U.S. as refugees from Iran. My brother was responsible for carrying our money. We had $5,000, and he put it in every pocket of his body … That’s neither safe nor secure."

Another bill inside the wallet was labeled "97" to represent the percentage of garment workers in Bangladesh who are paid in cash, with little or no accounting and protection against theft. For many workers, cash wages do not always come on time and managers may skim a little bit for themselves. These inconveniences and corruption can be erased by a verifiable digital payment direct to a personal account. Employers can also benefit from digital payments, which ensure more careful accounting and save them money by being more efficient than labor-intensive cash payments.

When it comes to inclusion in the formal economy, women experience more barriers than men. This is largely because cultural norms and policies can make it harder for women to obtain and manage their own accounts. In countries like India, poor people are putting cash savings into a household account that oftentimes does not permit women access. "It needs to be one account per adult to be considered financial inclusion," said Doug Pearce, Practice Manager for Financial Infrastructure and Access at the World Bank Group. Overcoming behavioral barriers, Pearce explained, is necessary to shift fully from a cash economy to a digital one, which could not only alleviate barriers for women but also make saving and managing finances safer by using mobile technologies.

Samuel Schueth, Technical Director at InterMedia, an organization that collects demand-side data to guide deployment and track usage of financial tools in developing countries, explained the financial inclusion gender gap while referencing the wallet’s "1.1 billion" bill, which represents the number of women – or 42% of the female population – who are excluded from the formal economy. “It’s defined as the percentage of men who have access to a financial services account minus the percentage of women. While it varies across metrics and country to country, the gap is closing for men but not for women.”

Inclusivity also depends on the degree to which governments address privacy and security challenges in the digital market. Victor Shiblie, Editor in Chief and Publisher of The Washington Diplomat, raised questions about the responsibility of governments to create safety valves that control outflows of money in the digital market. In the Western Hemisphere, many nations are concerned about new risks through digitization like cybercrime and rights to privacy and control of individual data. Offering a counter perspective, Najmi noted, “The concerns that many European countries and the U.S. hold around privacy and security are not globally shared.” For example, India created a digital locker where people keep core documents about themselves and personal identification because, in doing so, they can easily access and participate in government provisions and services.

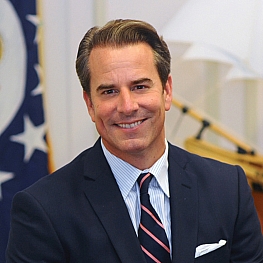

One of the convening session’s featured presenters, Olivia White, Partner of McKinsey & Co., elaborated on the importance of participation in assessing financial inclusion. McKinsey Global Institute’s new report "Digital Finance For All" (September 2016) has a more nuanced view of financial inclusion, which goes beyond the traditional notion of account ownership and delves into active use – saving, investing and borrowing. In many developing economies not everybody is financially included, certainly middle class people, but even wealthy people who rely on cash or do not have access to credit. In Pakistan, a country of 100 million people, there are under 250,000 mortgages. Realities like these demonstrated to White and her McKinsey team the need to assess macroeconomic benefits of digital financial services.

By 2025, increased use of digital finance could increase global GDP to $3.7 trillion. This equates to 1.5 times Africa’s GDP or is the same as giving $600 to every person in the emerging world. A more robust global GDP also drives job growth. The projection for new jobs generated because of increased financial inclusion is 95 million across emerging markets, White stated from the report.

Pearce, the other featured speaker in this session, addressed the World Bank Group’s role in enabling financial inclusion, specifically at the country level. He leads a team developing national financial inclusion strategies in 25 countries that represent 73% of the world’s unbanked. Operating under a goal of 1 billion new account holders by 2020, the World Bank helps these countries meet financial inclusion targets by working with authorities on reforms that prioritize and initiate financial inclusion through digital services. Pearce said the national scope of each strategy allows for better coordination of resources, which signals to the private sector an easier path to innovate and invest in financial services. The “FinTech,” or financial technology, trend for inclusion is already proving effective in countries like China and India, where 84% of the 1.43 billion new accounts from 2014 to 2015 were created.

As the world moves toward a borderless economy, the opportunities and implications of digital finance are also growing more nuanced. Puru Trivedi, Associate Director for Corporate Relations at Meridian, nodded to the intersection of finance and politics, specifically the recent demonetization of India’s currency as a move to force people off the illegal market and into the formal economy – but without fully considering the consumer implications. On the flip side, the digital marketplace could provide new opportunities for government subsidies, which a majority of the world’s poor and rural farmers rely on for survival.

From a system perspective, financial regulators will also need to begin thinking differently about their roles – moving beyond compliance to ongoing supervision. "In managing the digital economy, regulators can use digital tools to help customers gain more confidence in the system," Najmi purported. She explained how sending an SMS that acknowledges a customer’s submitted complaint, with a record number and response timeline included, would be monumental compared to the radio silence most people experience with the existing financial industry.

As more people around the world build trust in digital financial services, participation in the future digital economy will also grow. With a financial revolution upon us, people not governments will begin voting with their money about which countries are most hospitable to their economic future.

![Olivia White, Partner at McKinsey & Co., explains key findings in [TAG] McKinsey Global Institute’s new “Digital Finance For All” report (September 2016). She spoke to the more nuanced view of financial inclusion, which goes beyond the traditional notion of account ownership and delves into active use – saving, investing and borrowing. The report assesses the macroeconomic impact of digital financial use, which could increase global GDP to $3.7 trillion by 2025. This equates to 1.5 times Africa’s GDP or giving $600 to every person in the emerging world.](https://www.meridian.org/wp-content/uploads/2016/12/Olivia-White_4-FB.jpg "Olivia White, Partner at McKinsey & Co., explains key findings in [TAG] McKinsey Global Institute’s new “Digital Finance For All” report (September 2016). She spoke to the more nuanced view of financial inclusion, which goes beyond the traditional notion of account ownership and delves into active use – saving, investing and borrowing. The report assesses the macroeconomic impact of digital financial use, which could increase global GDP to $3.7 trillion by 2025. This equates to 1.5 times Africa’s GDP or giving $600 to every person in the emerging world.")

See More Photos

Speakers

Project Partner

Staff

Project summary

| The digital finance download: Diplomats and journalists explore the data driving financial inclusion in the future global economy | November 2016 | |

|---|---|

| Number of Attendees: | 22 |

| Regions: | Europe and Eurasia |

| Countries: | Denmark, Armenia, Albania |

| Impact Areas: | Media and Journalism, Security and Defense |

| Program Areas: | Diplomatic Engagement |

| Partners: | NGOs |